Delivering Value through Inclusive Growth

Dalmia Bharat Limited today announced its audited consolidated financial results for the year and Quarter ended March 31, 2016

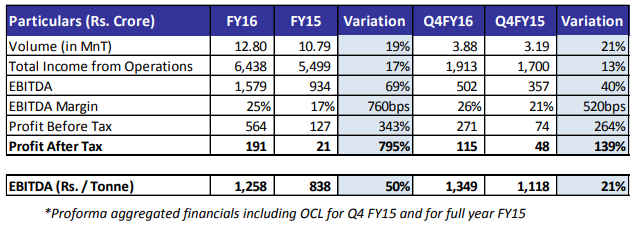

Annual Performance

Total Income from operations for the year is up by 17% to ₹6,438 crore as against ₹ 5,499 crore for the previous year led by increase in sales volume by 19% YoY as against industry’s growth of 5.3% in FY16.

The Company earned an EBITDA of Rs. 1,579 cr vs. 934 cr in FY15, up 69% YoY. EBITDA margin for the year under review improved to 25% as against 17% for the previous year led by better brand positioning, improved sales volumes and cost optimization.

Variable cost on per tonne basis for the year has witnessed reduction of 14% to ₹ 1,351 from ₹ 1,562 as compared to previous year. Our continuous focus towards sustainability has resulted into significant savings. Power consumption/T of cement produced has reduced to 67 kwh in FY16 from 71 kwh in FY15. Blended cement as a percentage of total cement production has increased to 80% in year under review vs. 74% last year.

Power & Fuel cost for the year on per tonne basis was ₹ 649 was lower by 27% YoY led by continuous drive to use most economic fuel and improvise heat efficiency. Non fossil fuel usage increased to 73% in FY16 vs. 45% in FY15. Fixed Cost per tonne witnessed reduction by 15% YoY driven by cost focus and improved capacity utilization.

Quarterly Performance

The Group sold volume of 3.9 MnT and earned EBITDA of Rs. 502 cr, highest ever for the quarter, up 40% on YoY basis. EBITDA on per tonne basis for the quarter was ₹ 1,349, up by 21% YoY and 13% QoQ

EBITDA margin for the quarter improved to 26% as against 21% in Q4FY15.

Variable cost on per tonne basis has been the lowest ever reported by Dalmia at 1,185. This has been a resultant of savings realized from drop in fuel prices, increased use of non-fossil fuel and enhanced power efficiencies.

Non fossil fuel consumption increased to 82% as compared to 76% in Q3FY16 and 61% in Q4FY15. This is furtherance to our commitment of optimizing costs by adopting low cost fuel strategy.

Efficiency improvement Initiatives led to reduced Power consumption/T of cement for the Group. It has optimized to 64 kwh as compared to 68 kwh in Q3FY16 and 69 kwh in Q4FY15.

Significant Developments

Commercial production has commenced at Belgaum, Karnataka w.e.f 31st March, 2016 During the quarter, Dalmia Bharat Limited increased its holding in subsidiary company Dalmia Cement (Bharat) Limited from 85% to 100% by allotment of 75,00,000 equity shares of Rs. 2 each @ Rs. 825 per share for consideration other than cash. The total number of outstanding shares increased to 8.88 cr shares with paid up capital of Rs. 17.8 cr.

Outlook

We have witnessed improved cement demand since second half of FY16.

We expect rural demand to gain momentum in addition to the infrastructure growth. The central Government is committed towards development of rural areas and progress of farmers.

Our strategy of strengthening the brand and continuously improvising on efficiency parameters has created opportunities. Our goal is to continuously enrich our operations and performance.