Press Release for the Quarter ended December 31, 2014

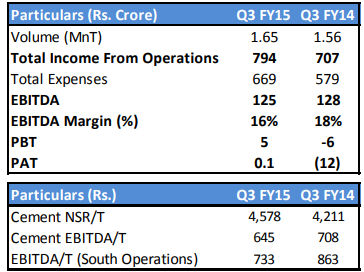

Sales Volume – 1.65 MnT

Total Income From Operations - Rs. 794 crore

EBITDA – Rs. 125 crore

Dalmia Bharat Limited today announced its financial results for the quarter ended December 31, 2014.

The acquisition of Dalmia Cement East Limited (formerly Bokaro Jaypee Cement Limited) was consummated during the quarter with 100% stake in the company, now wholly owned subsidiary of Dalmia Cement (Bharat) Ltd. The total enterprise value for the same is Rs. 1,150 crore. The quarterly results under review include financials of Dalmia Cement East Limited w.e.f. 16th November, 2014

Total Income from operations was Rs. 794 crore for the quarter as against Rs. 707 crore for the corresponding period of previous year, led by increase in volumes (+6%) and sales realizations (+9%).

EBITDA for the quarter was flat at Rs. 125 crore. Power & fuel cost on per tonne basis was lower by 16% on YoY basis but the same has been offset by higher freight cost and slightly increase in raw material cost for North East Operations.

PAT for the quarter was positive at Rs. 10 lakhs as against loss of Rs. (12) cr. in the corresponding quarter of the previous year.

Southern Operations:

Variable Costs on per tonne basis were lower by 4% on YoY basis for the quarter on account of further enhancement in efficiencies. Our Power consumption per tonne of cement produced has improved to 69.5 kwh as against 71.3 kwh and fuel cost on calorific value basis has witnessed a reduction of 16%. Freight costs were higher during the quarter but we expect the same to recede in coming quarters on account of drop in crude prices.

North East Operations

North East Operations witnessed stabilization of operations during the quarter. Volumes were up 22% on QoQ basis and EBITDA improved significantly on YoY & QoQ basis.

Associate Company:

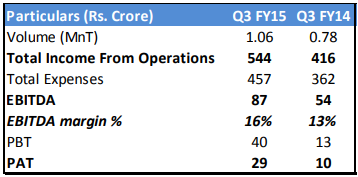

OCL India limited - Financial Performance

Cement Outlook

The macro economic factors are improving and expected to improve further. With higher GDP growth, impetus on ‘Make in India’ strategy and further rate cuts expected, industrial production expected to improve, resulting in improved cement demand. Improved demand and rationalization of capacity additions, would also lead to improved Capacity Utilizations.